Five years ago, generative Artificial Intelligence (AI) was something many students were only beginning to encounter in search engines, chatbots, or viral online demos. Now it shapes everything from hiring plans, utility forecasts, office software budgets, and the balance of power inside the technology sector.

Stanford’s 2025 AI Index shows how fast this spending has accelerated: U.S. private AI investment reached $109.1 billion in 2024, global private investment in generative AI hit $33.9 billion, and 78% of organizations reported using AI in the same year, up from 55% the year before. Firms began spending heavily on models, chips, cloud capacity, and data centers in the belief that AI could raise output and cut operational costs. Globally, now, those costs have risen to levels that demand measurable returns for investors and firms.

On top of the need for results, the surge in AI adoption holds a more complicated economic problem, asking not if AI can increase productivity, but what kind of economic structure is forming around it. As companies invest heavily in AI, the market around AI systems is becoming more expensive, more physically demanding, and more concentrated in the hands of firms that control computing power, distribution, and customer access. The result is a market defined not just by innovation, but by a contest over who captures the gains and who absorbs the risks.

ChatGPT currently leads the market because OpenAI turned Large Language Models (LLMs) into something millions of people can use without technical training. That consumer breakthrough became a business one. OpenAI said in late 2025 that more than 1 million business customers were paying to use its products, either through ChatGPT for work or through direct model access. Executives are buying these systems expecting faster software development, cheaper customer support, and higher output from the same headcount.

OpenAI opened the field, but the next question is how much of the economic upside it can keep. Anthropic (Claude), Google (Gemini), and Microsoft (Copilot) are all trying to capture the spending wave ChatGPT helped start, though they are not competing for the same services. OpenAI has built an “everyman’s” product that millions of users visit and use as an entry point into AI. Google and Microsoft are pushing AI through software ecosystems that companies already depend on. Anthropic has gained ground, selling reliability and coding strength to enterprise buyers.

What looks like a battle over chatbots from the outside is, inside boardrooms, a fight over contracts, software access, how developers work, and which AI tools become foundational to which corporations.

For students, AI’s economic reach is already visible in daily habits. Darius Ashrafi (‘27) said AI has become a normal part of his routine. “I honestly use AI pretty often; it’s become the norm now,” Darius said. “I’d say I use it almost every day actually.”

Darius said he mainly uses AI as a research tool for school, but also increasingly turns to it outside the classroom. “It makes my job easier too,” he said. “It’s slowly but surely replacing Google.” That shift shows why AI companies are not only competing for corporate contracts, but also for the habits of future workers, consumers, and students who may begin treating chatbots as basic tools for finding and organizing information.

Despite prolonged AI usage being commonly linked to a decline in critical thinking abilities, its short-term performance boost is real. A 2023 study on the productivity effects of AI suggests it can improve performance in bounded tasks, such as drafting documents, summarizing information, assisting programmers, and handling customer interactions. Those uses save time and may lower labor costs for specific functions. But there is a real gap between proving usefulness in independent workplaces and proving economy-wide transformation.

Companies are now spending heavily on AI because they believe it will eventually raise output, cut costs, or keep them from falling behind rivals. Those spending decisions are effectively bets on future returns. Some firms may turn early gains into lasting profit, while others may find that the costs of adoption outweigh the benefits. Stanford’s data can capture the velocity of adoption; however, it does not tell you which of these bets will pay off.

Competition complicates the economics. If model quality diffuses and more firms can offer capable systems, pricing power weakens. That is good for buyers and punishing for firms that need very high margins to justify enormous datacenter and production bills.

Stanford found that leading open-weight models (who make their internal settings [parameters] available for others to use, adapt, or build on) narrowed the performance gap with closed models (who make their internal settings private) sharply throughout 2024. If strong enough models become cheaper and more available, the competitive advantage shifts away from pure model quality and toward reach, access to computing power, and business ties, which helps large companies that already control how customers are reached.

That shift creates a broader problem where optimism about AI confronts a harder fact about industrial power. The market looks crowded at the user end, but the core aspects remain concentrated. The Federal Trade Commission’s 2025 report on AI partnerships warned that deals between major cloud service providers and AI developers can give the largest firms equity rights, revenue sharing, consultation rights, and other forms of leverage that shape who gets access to infrastructure and on what terms. In practice, those terms can strengthen the biggest firms by giving them more control over financing, infrastructure access, and strategic decisions, while leaving smaller competitors with less room to grow.

A sector can look competitive on the surface and still be imbalanced underneath. If a small number of firms control the computing backbone, it becomes more expensive for new companies to enter the market and harder for developers and business customers to switch providers. The winners then gain an advantage that has less to do with product quality than with who got there first and closed the pipelines.

Labor is where the consequences of AI land closest to many people. The International Monetary Fund (IMF) estimated in 2024 that almost 40% of jobs worldwide are exposed to AI — meaning that a significant share of their tasks could be altered, assisted, or automated by AI — with exposure rising to about 60% in advanced, first world economies.

However, exposure is not the same as job loss, and the IMF suggests that in some cases, AI can even complement some exposed jobs rather than replacing them. Even so, exposure at that scale means firms now have a credible way to redesign white-collar work, especially the routine parts of analysis, drafting, support, and review.

That matters most for people entering the labor market over the next several years. Entry-level knowledge work has traditionally been where workers learn by doing the simpler tasks first. If those tasks are automated, the career ladder does not disappear entirely, but several lower rungs do, as companies will save money by removing these positions.

For Ryan Shi (‘26), a graduating senior, AI’s effect on students is tied directly to how prepared they will be for college and future jobs. Ryan said AI should become a basic learning tool, but only if students learn to use it without handing over the thinking process. “Students should know how to be able to use it effectively without just completely offloading all the work onto AI,” Ryan said.

That distinction matters for students entering a labor market where AI may handle more routine drafting, review, and problem-solving tasks. Ryan said the real value of AI is not that it can replace student effort, but that it can create fast feedback loops. Students can use it to get explanations, check mistakes, and revise their work more quickly, especially when a teacher or expert is not immediately available.

Still, Ryan said those benefits depend on students having enough knowledge to evaluate what AI produces. “You don’t just want to take whatever AI says verbatim,” Ryan said. “You want to be able to think critically about what it’s saying for yourself and check it for mistakes because AI does make mistakes.” In that sense, AI may not eliminate the need for strong workers, but it could change what makes someone valuable: the ability to question, verify, and improve machine-generated work.

Ryan said his main takeaway is that AI is effective as a support tool, but should not be used “as a substitute for real thinking and cognitive effort or as a substitute for basic subject knowledge.”

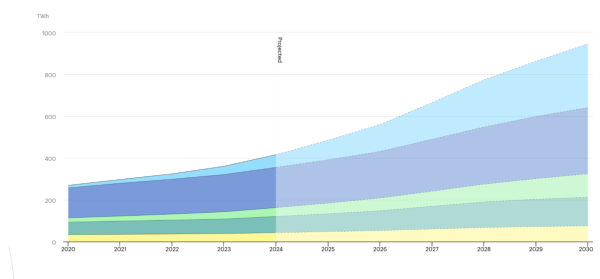

The physical economy is absorbing the shock, too. The International Energy Agency (IEA) projects that electricity demand from data centers will more than double by 2030 to around 945 terawatt hours, enough energy to power ~92 million average American homes for a year, with AI as the main driver.

The AI market is no longer just a software issue; it’s also a power issue, a land use issue, a construction issue, and in some regions, an energy grid stress issue. Every confident claim made by groups such as the World Economic Forum about AI-driven growth now runs into a physical constraint: Will the infrastructure be built fast enough? Will utilities supply the demand? Who will pay for the upgrades?

Ms. Kaitlin Ritsema, a chemistry and environmental science teacher, said students often miss the physical systems behind AI because the tools feel digital and invisible. “For AI usage, specifically, the main environmental impacts are related to the need for large amounts of cooling water, increased electricity generation and a multitude of raw materials needed for the infrastructure supporting AI,” Ms. Ritsema said.

Ms. Ritsema said water demand is one of the clearest examples. Even when electricity comes from sources such as nuclear power, fossil fuels, or some solar technologies, cooling water can still be part of the system. “Large amounts of freshwater needed strain water needed for other things, like agriculture and public supply,” she said.

Ms. Ritsema also pointed to the material side of AI growth. Mining for hardware components can create land use change, water and air pollution, and species disturbance, while also raising supply chain concerns. “Every element needed has a story that could be analyzed,” she said. “Where is it coming from? How is it being mined and produced? How is it being transported? Can it be recycled?”

Still, Ms. Ritsema said AI should not be treated as an isolated environmental problem. “AI is only one piece of this larger puzzle,” she said. In her view, the environmental debate over AI should push students toward a broader understanding of how everyday technologies depend on energy, water, land, and raw materials.

The market has also become riskier in ways firms cannot ignore. Errors, privacy problems, copyright disputes, and false content all create real costs. If firms must pay more for legal access to data, test their systems more carefully, or change products to avoid lawsuits, profits shrink. If customers do not trust AI in important settings, they may use it less or confine it to simpler tasks.

Economics Teacher Damon Halback said the current AI economy reflects both concentration and competition at once. “The current AI market structure is an interesting combination of an oligopoly in the retail market and a monopolistically competitive enterprise market,” Mr. Halback said. He explained that while consumers mainly see a handful of dominant firms with the infrastructure to serve mass demand, the enterprise side includes many narrower, specialized firms competing on price, service, and application.

Mr. Halback also noted that the infrastructure required to compete at scale is so expensive that “there isn’t room for small companies in the retail marketplace.”

He continued that one of the clearest signs to watch is whether AI produces measurable productivity gains rather than just excitement and spending. “Typically, you would look at a productivity indicator,” he said, pointing to sources such as international productivity measures and the U.S. Labor Productivity Index.

At the same time, he cautioned that those indicators lag behind real-time developments, while many AI firms are still losing large amounts of money because of capital investment. For now, he suggested, the returns are more obvious for infrastructure providers than for the companies building the models themselves.

On labor, Mr. Halback said the disruption may hit jobs that had once seemed more insulated from automation, including “jobs that require significant investment in education and include asymmetric tasks.” In his view, firms may increasingly use AI to handle novel situations once reserved for trained workers, creating the risk that “educational investments might be misaligned with the upcoming labor market.”

He also argued that AI’s gains are unlikely to be distributed evenly. “It seems most likely that AI will increase inequality,” Mr. Halback said, explaining that the largest benefits may go to people and firms that already possess educational, social, and financial advantages. If that pattern continues, AI may not simply raise output. It may also deepen existing divides in access, labor market outcomes, and opportunity.

The current AI market is a test of whether massive private spending can produce durable productivity gains without deepening concentration and labor insecurity along the way. Firms are racing to become the operating layer for AI work. Infrastructure owners are gaining leverage while energy demand is accelerating. Employers are reconsidering what kinds of labor they actually need. The gains may be real, but this is economic restructuring in progress, and the winners have not yet been decided.